Rice export ban:Why India is so crucial to global rice trade

2023-07-20

The commodity trading industry has enjoyed an upward trend over the past five years. While all industries go through multiyear cycles of peaks and troughs, the industry’s prospects look excellent for the years ahead.

Indeed, commodity trading is on the cusp of the next normal. The energy transition now under way is an economic and physical transformation that cuts across and integrates the various global food, energy, and materials systems. From a commodity trading standpoint, this transformation will increase structural volatility, disrupt trade flows to open new arbitrages, redefine what it means to be a commodity, and fundamentally alter commercial relationships. All these developments will create unique opportunities and challenges for new and incumbent players alike.

In this article, we explore the trends underpinning commodity trading value pools, discuss five success factors and their potential implementation, and present our perspective on the three business models that could develop over time.

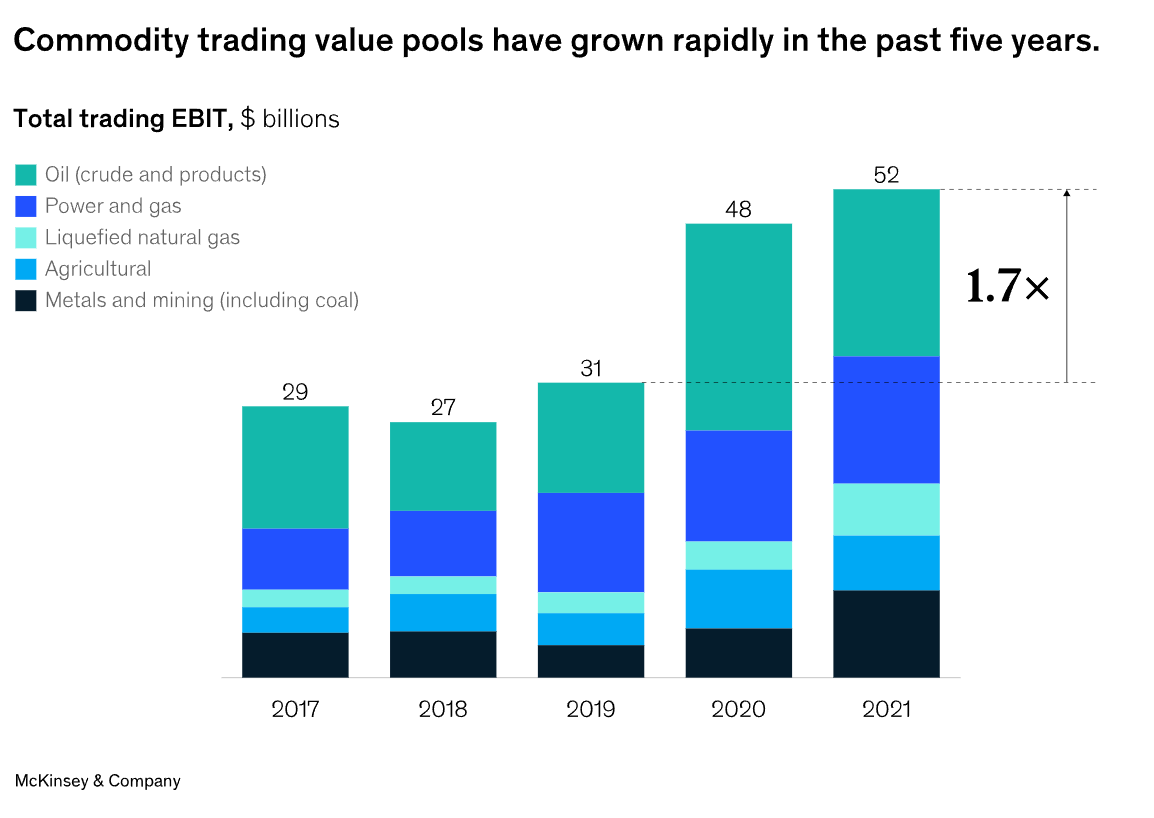

Commodity trading value pools have grown substantially, almost doubling from $27 billion in 2018 to an estimated $52 billion of EBIT in 2021 (Exhibit 1). The majority of this growth was fueled by EBIT from oil trading, which were estimated to have increased by more than 90 percent to $18 billion during this period. Power and gas trading was just behind, rising from $7 billion to $13 billion. These value pools maintained their upward trajectory in 2022. The market will likely attract new entrants that enhance competition, and our analysis suggests that its overall value will continue to grow.

We identified four developments that contributed to this rapid growth and will have an impact in the years to come.

While significant economic and environmental benefits could be captured from decarbonization, the inconsistency of incentives, bottlenecks in the value chain, and current geopolitical turbulence have clouded the supply and demand picture. Annual investments in traditional hydrocarbons have dropped by 50 percent since 2013, but the level of funds committed to the energy transition—approximately $700 billion in 2021, about one-third the $2 trillion needed in 2022—will likely not be sufficient to prevent the emergence of sustained bottlenecks.

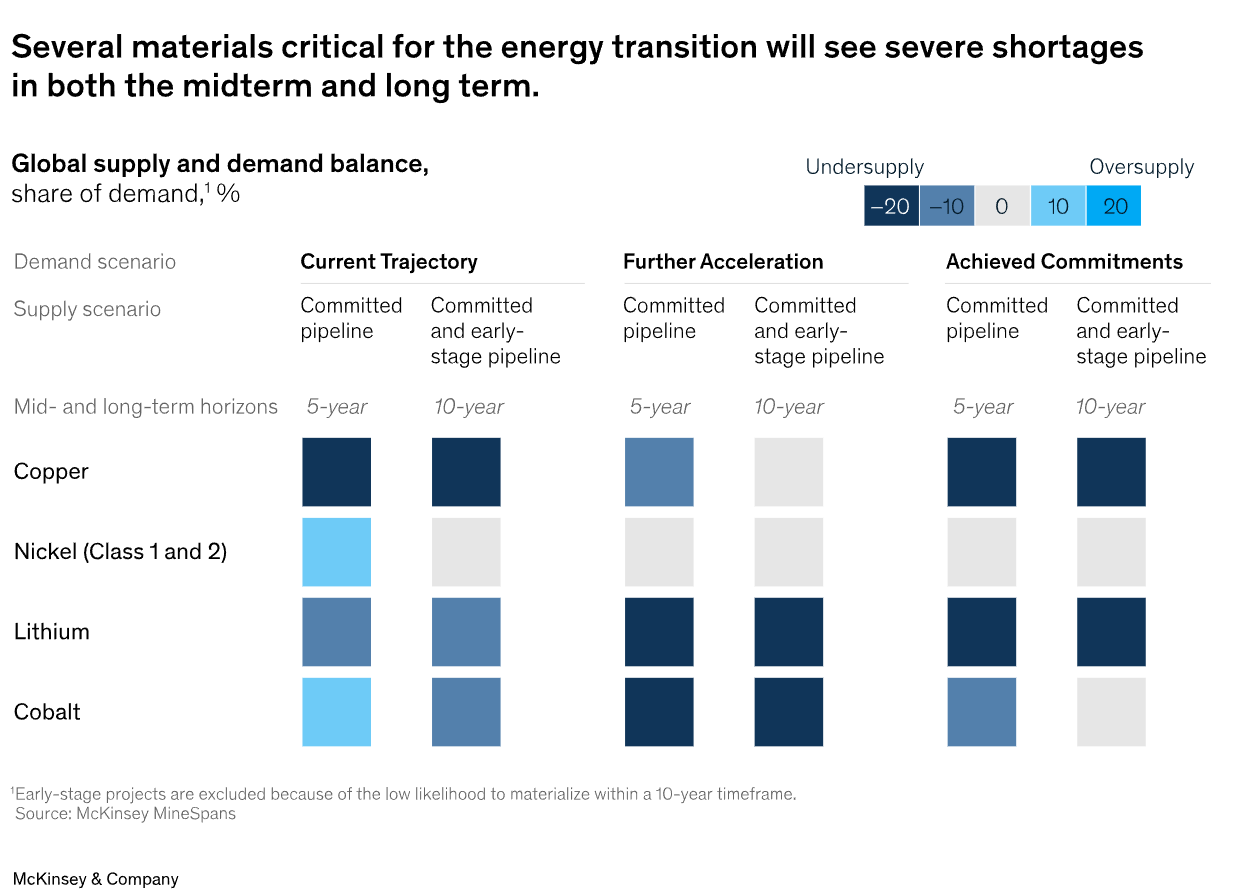

Without significantly building out the underlying supply chain, our analysis projects potential supply imbalances (Exhibit 2). For example, lithium and nickel have a high probability of supply constraints by 2030, particularly in the Further Acceleration and Achieved Commitments scenarios discussed in McKinsey’s Global Energy Perspective 2022.1 Similarly, in Germany and Italy alone, the land space currently occupied by renewable-energy sources (RES) would need to double by 2030.2 These supply gaps are also being observed outside the power space: continued feedstock supply constraints—combined with increasing demand from refineries on the back of regulations favorable to second-generation biofuel feedstocks—have increased used cooking oil (UCO) prices by 90 percent in the past 18 months.3

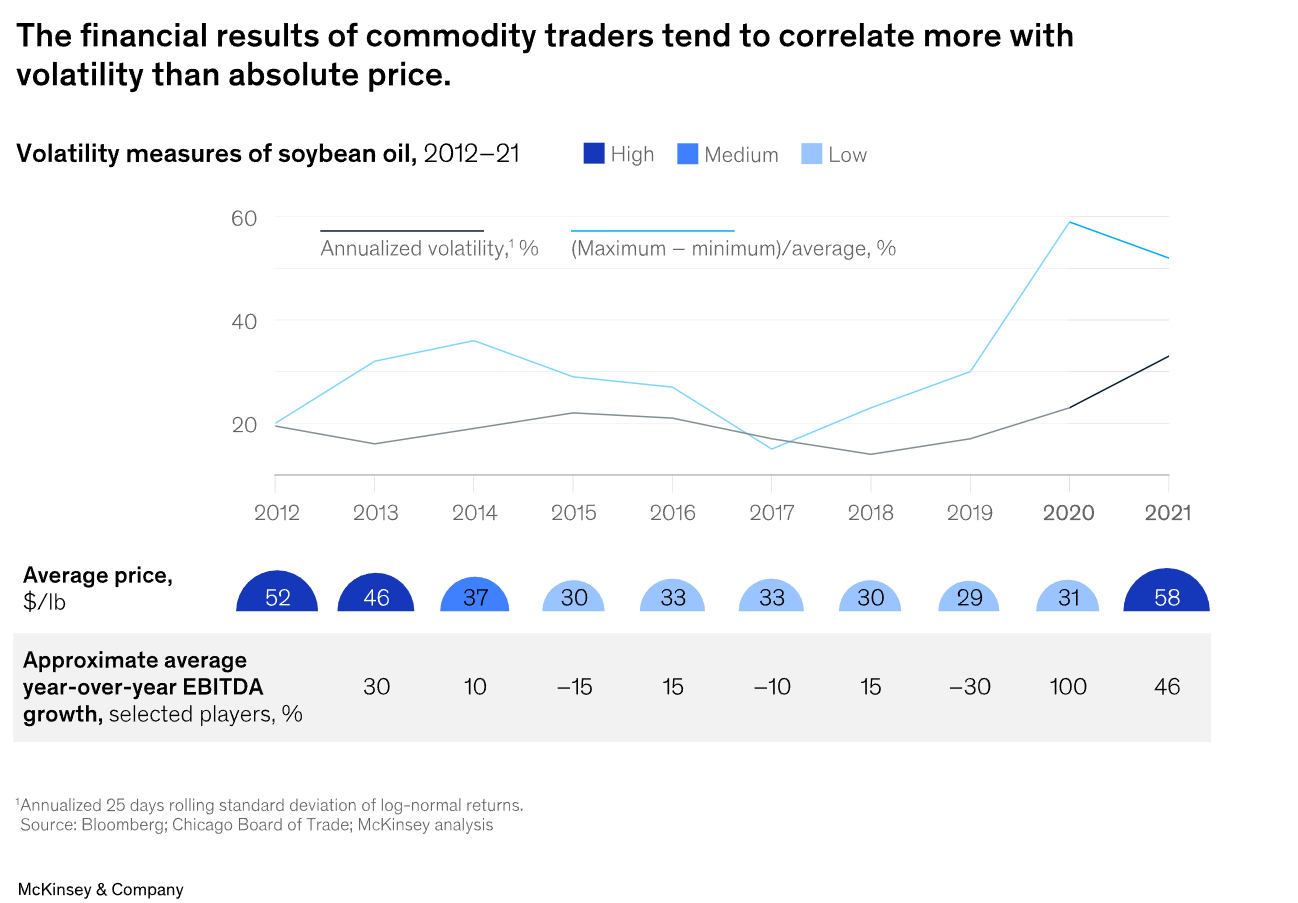

The increased susceptibility of markets to both short- and long-term volatility and boom-and-bust cycles will likely increase the value of maintaining prompt inventory to deploy in response to a market dislocation. Over the past two years, markets have experienced historic spikes caused by COVID-19, severe weather, geopolitical events, and macroeconomic uncertainty. These fluctuations have been most apparent in the energy sector, but other commodities have also been affected. For example, because producers of agricultural goods and metals use energy as an input, volatile prices have upended the economics of production and led to shutdowns. The historical volatility of US natural-gas prices (as measured by Henry Hub natural-gas spot prices) jumped from a low of 25 percent in the third quarter of 2021 to 179 percent just six months later. European gas prices (as measured by Dutch title transfer facility prices) increased from less than €10 per megawatt-hour (MWh) in the second quarter of 2020 to more than €330 per MWh in the second quarter of 2022. This spike has led fertilizer companies to halt Europe-based production and exports. From a commodity trader’s perspective, profitability is determined by a combination of price levels and price volatility (Exhibit 3).

Given these expectations of higher volatility, flexible capacity to respond to changing market conditions will become more critical from both balancing and economic standpoints. Our analysis indicates that achieving a global electrical supply based on 70 percent intermittent penetration in 2050 would require an embedded flexible capacity of 2.5 times at 25 percent penetration. Players could capture considerable economic value by optimizing flexible assets, which could account for more than 60 percent of the overall commodity trading value pool.

However, estimating the value of this flexibility based on forecasts is challenging—especially when physical assets are subject to operational, regulatory, or environmental constraints. For instance, most business cases for flexible assets do not factor in the occurrence of extreme market scenarios that are likely to occur over their 30-year lifespan, thereby underestimating the potential economic rent.

Moreover, the energy transition has priced environmental impact into the supply curve, which will have implications for market volatility. A reordering of asset values and cross-commodity relationships would more strongly intertwine the price volatility of traditional commodities with that of new green commodities—and vice versa.

The flow of global commodities remains vulnerable to potential disruption from one-off events.

The COVID-19 pandemic is a case in point: the precipitous drop in demand for oil and the corresponding decline in seaborne crude-oil-pricing benchmarks, such as Dubai Fateh, saw charter rates for very large crude carriers (VLCCs) trade at $150,000 to $200,000 a day in the first quarter and second quarter of 2020, with tankers anchored off the coasts of major import centers to provide floating storage.

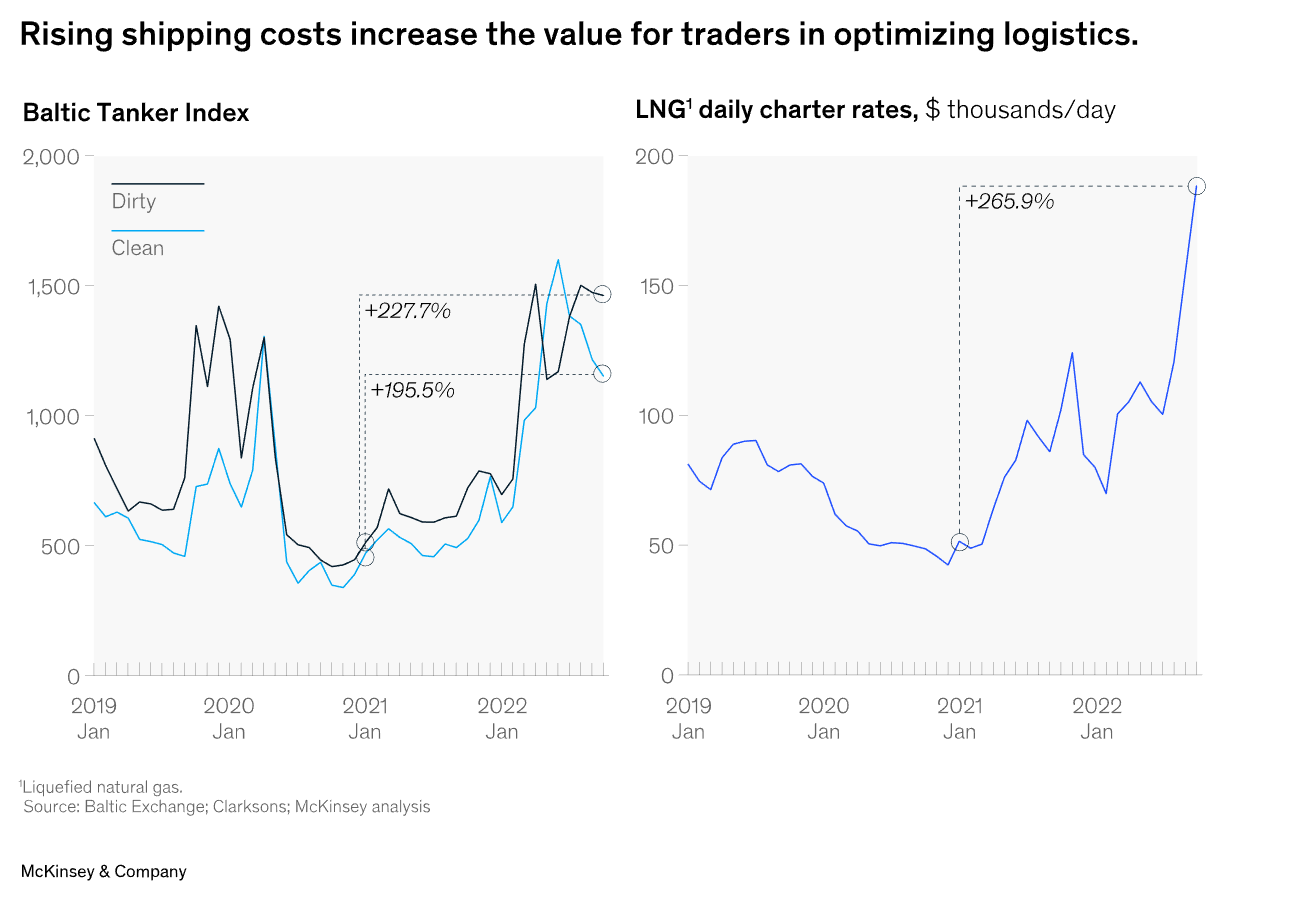

Recent events have kick-started a reordering of global flows, and the geographical distribution of relevant and competitive assets makes a reversion to pre-2021 levels unlikely in the foreseeable future. In energy, the reduction in Russian supplies to Europe and its allies has led the European Union to rely on imports sourced or rerouted from longer distances, such as Latin America, the Middle East, the United States, and West Africa. Conversely, Russia is exporting higher volumes farther afield, including to China and India. As a result, ships will likely spend more time at sea, and freight optimization could have a greater impact on margins. For example, shipping costs have risen dramatically since the first quarter of 2021: Baltic dirty, Baltic clean, and liquefied natural gas (LNG) tanker rates have increased by approximately 228 percent, 195 percent, and 266 percent, respectively (Exhibit 4).

For agricultural commodities, the invasion of Ukraine has severely disrupted exports from the Black Sea, a region responsible for large shares of the global trade in wheat (25 to 30 percent), corn (around 20 percent), and sunflower oil (more than 50 percent). This disruption is having knock-on effects on other agricultural exporters that are already affected by drought and price inflation, leading them to limit flows to maintain food security. The resulting sustained volatility in commodity prices has enabled traders with access to physical alternatives to capture significant value—for example, by rerouting flows, optimizing freight, leveraging storage assets, and blending commodities to customer specifications.

More severe trade flow disruption scenarios could occur, including the potential formation of trade blocs, with the impact felt differently by each commodity class. In one scenario, for LNG, Russian exports could be wholly excluded from OECD markets, shifting instead to China, India, and Türkiye (Exhibit 5). To plug the supply gap, Australian and North American supplies would be redirected to Europe, even though some national oil companies (NOCs) have maintained that it is their obligation to deliver on supply commitments. Europe could seek to severely limit demand because projected global liquefaction capacity is insufficient to completely replace Russian volumes. Despite this “bloc building,” energy flows will adjust to balance the system, and these flows will remain strongly interlinked via fundamental pricing relationships. In the case of metals, however, it is possible that geopolitical factors could override economic relationships and significantly regionalize trade flows (for example, in the battery value chain).

This reliance on longer distances and rerouting will further constrain the shipping market. Furthermore, the changes in trade flows will require traders to reevaluate their downstream exposure—a particularly relevant consideration for those with European refining assets as the continent increases imports of diesel. Other traders would have to determine how to meet their customer commitments.

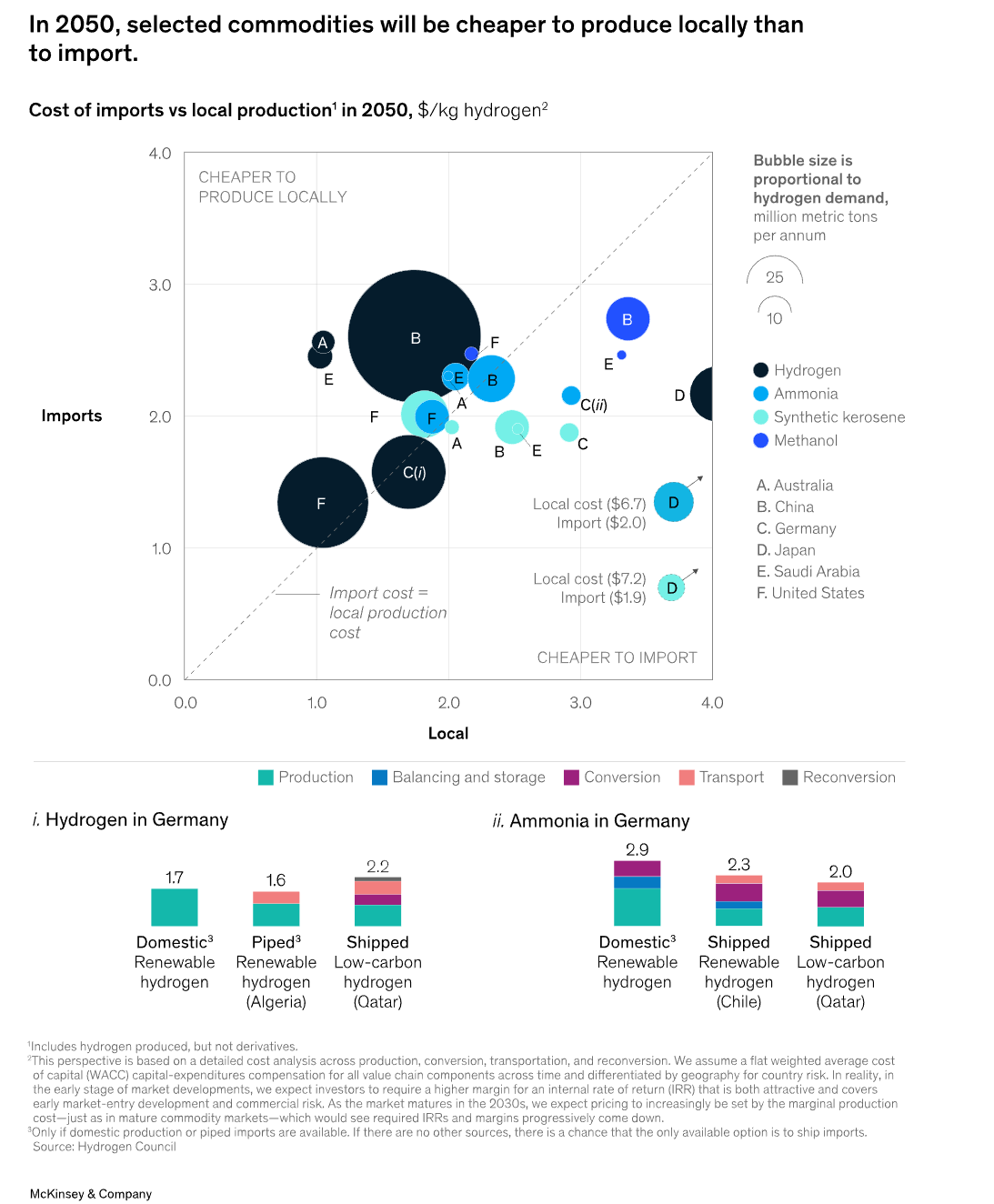

Over the long term, the energy transition could contribute to more regionalization. As the world moves to electrification and alternative fuels, underlying cost structures could create incentives for more local and regional supply networks and in turn reduce traditional large-volume, long-distance commodity flows for oil, coal, and LNG. Even with a potential move toward regionalization, global trade flows would still likely be required to balance energy systems in the foreseeable future. One example is hydrogen: a number of high-demand countries could rely on their own hydrogen production and consumption because transportation and the avoidance of converting and reconverting derivatives can be a significant contributor to overall unit economics (Exhibit 6).

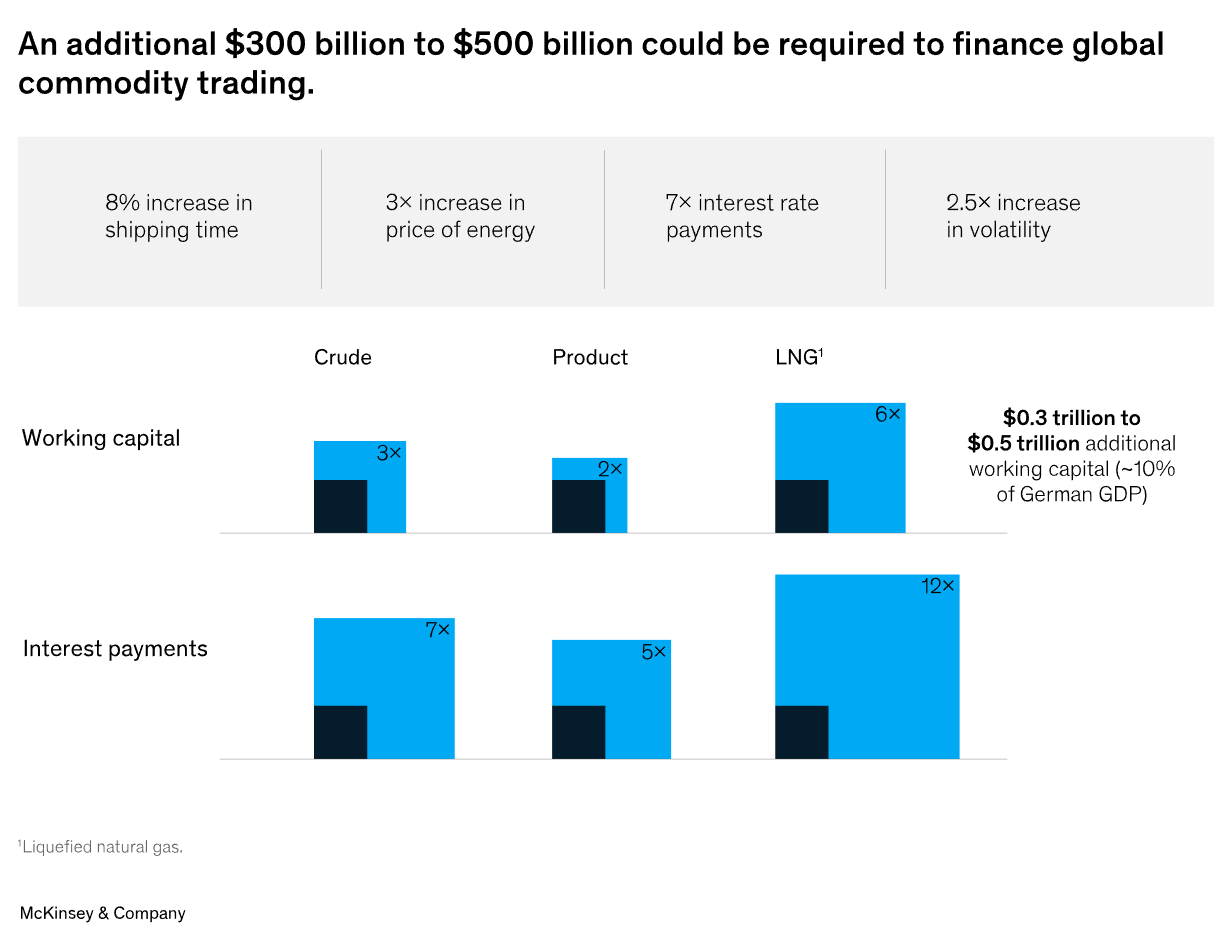

The volatility of spiking commodity price levels has significantly tightened collateral requirements and increased the size and frequency of margin calls. Working capital requirements could rise by 1.5 to 3.0 times the current levels depending on the commodity. In power and gas, for example, price volatility has limited the scope of positions for market participants. According to estimates, energy margin calls could total $1.5 trillion.

In other commodities, the stance of central banks has resulted in a rapid increase in the cost of trade financing for various commodity traders and created a massive challenge for players, especially small and medium-size commodity traders. In the past six months, financial intermediaries have significantly reduced credit to Asia-based metal traders, which have responded by restricting trading activities, exploring selective asset sales, and shoring up balance sheets to maintain access to working capital and to avoid financial distress. Traders with large portfolios and healthy balance sheets have taken advantage of these restrictions to increase their margins considerably. The added working capital requirements combined with the longer shipping times could further increase the competitive advantage of large traders (Exhibit 7). However, it also creates a potential opportunity for larger traders to emerge as “financiers of last resort” for smaller players. For instance, in energy transition commodities such as copper, merchant traders have engaged junior miners on long-term origination contracts linked to prefinancing.

In the past five to ten years, commodity markets have experienced a dramatic rise in the overall level of liquidity. While the past two years saw events such as the drop in liquidity in European power and gas trading, any repercussions are unlikely to affect the overall trend. One major factor has been large producers that moved from direct-to-consumer (D2C) sales into trading to capture more value from their global logistics, systems, and inventories. Similarly, some large customers could shift away from long-term contracts (LTCs) to capture benefits from the spot market. For example, Middle Eastern NOCs have increased margins by bringing their product into the traded markets. Commodity players have also enhanced their participation in one another’s value chains, such as energy traders taking part in the value chains of agricultural traders and vice versa.

Recent market developments include increased price transparency, greater access to structured and unstructured data (such as satellite imagery and infrared detection), contract standardization, new exchanges and platforms, and regulations. The resulting lower barriers created a virtuous circle, with higher market participation, transaction volumes and costs, and speed to market. An example is the LNG market, in which spot transactions account for more than 38 percent of annual volumes today (approximately 140 million metric tons) compared with 27 percent (approximately 60 million metric tons) in 2010. The monthly Japan/Korea Marker (JKM)4 futures open interest on the Intercontinental Exchange (ICE) has grown from 1,500 lots six years ago to more than 120,000 lots today, reflecting the increased liquidity of benchmark indices. And while the recent volatility has created incentives for customers to revisit LTCs, the growth in overall volumes will likely ensure that absolute short-term volumes increase as well. In iron ore, for example, the market is developing forward curves to help better manage flat-price and basis risks; the open interest in Singapore Exchange iron ore futures expiring up to three months out has more than doubled in the past five years.5 The net effect of these changes: the addressable market for all commodity flows continues to rise.

To capture opportunities, commodity traders will likely need to invest in new capabilities. Our analysis has identified five factors that could be critical to success in the years ahead.

The energy transition is redefining the commodity asset class with the arrival of new offerings being differentiated by geography, production methods, regulatory treatment, and environmental impact—and therefore being valued differently by customers. The development path of these new commodities will be determined by customer needs, willingness to pay, and the improving economics of new technologies that will enable differentiation for each commodity to a varying degree. Traders that have access to customer short positions and the accompanying customer-backed perspective could capture an advantage in originating and tailoring high-quality products (a clear differentiator in the metals space); anticipating and locking in demand; gaining insight into product differentials (specifically green-product price discovery); understanding value chain bottlenecks; and strategically shaping customer behavior.

Customer centricity is particularly relevant for new commodities such as sustainable aviation fuel, for which the lack of a wholesale market in the near term will make the D2C model (in which a single customer or a few large ones purchase a producer’s whole supply) the only model able to off-load exposure. Since customer centricity can be successfully developed independent of asset intensity, companies that have not historically focused on end customers would have to adopt a significantly different operating model, culture, and set of capabilities. Failure to adapt could leave margins for big commodity trading players, severely undermine the economic viability of asset investments, or both. Players must pay attention to their counterparty risk because larger customer exposures could create risks.

For example, demand for corporate power purchase agreements (PPAs), which has grown considerably in the past five years, will be spurred by the evolution of customer groups whose decarbonization needs cannot be met solely by pay-as-produced PPAs.6 This trend has created a need for 24/7 PPAs that can contractually specify the level of clean supply–demand matching, time and geographical granularity, the addition of renewables, and clean dispatchable capacity based on customer needs.

The current market environment has heightened how customers perceive risk. Many are pursuing LTCs. Even though these products don’t reduce risk significantly, they enable customers to lock in a price mechanism and secure supply. Producers will revert to short-term markets because their shareholders will not accept the negative impact from the loss of flexibility, the neglect of arbitrage opportunities created by short-term volatility, and the high costs of hedging illiquid long-term positions. Conversely, the high premiums commanded by producers and potential large mark-to-market write-downs will also steer customers back to short-term markets. That said, no model can accommodate all customer needs, and regional or commodity-specific nuances could slow the move to short-term markets. The LNG market is an example of regional nuances: European buyers are leaning toward short-term contracts, while those in Asia and Latin America are likely to prefer LTCs with some degree of flexibility. Moreover, producers may still rely on LTCs to make projects bankable and take final investment decisions (FIDs). A potential outcome could be a world in which short-term volumes remain robust and price indexes are recalibrated to more liquid and stable benchmarks.

With respect to new commodities, producers will likely need to maintain the ability to ramp up and down—a responsiveness that will be challenging if they are constrained by offtake agreements. For example, our evaluation of Power-to-X (for example, Power-to-Hydrogen) projects finds that fully merchant projects can offer a superior risk/return trade-off compared with fully contracted ones. The better result, which derives from the ability to switch between producing and selling power and hydrogen based on short-term market conditions, will, over time, encourage commodity players to return to short-term markets.

Therefore, to avoid impeding the energy transition, producers of new commodities could likely move faster to short-term markets compared with those of commodities such as LNG and power. The large, global players are well positioned to benefit from this trend, given that their diversified portfolios and balance sheets enable them to take on the long-term merchant risk associated with asset investments while participating in the short-term markets.

End customers that want to mitigate the environmental impact of their consumption could increasingly demand green products in various forms. Commodity players with an understanding of the green premium will be able to unlock arbitrage opportunities—for example, through adjustments to their product blending and logistics processes or through cost optimization. The green premium’s evolution and the opportunities it creates for players will be closely linked to how voluntary and compliance carbon markets evolve in the future. Although these markets will expand massively (coverage is expected to more than double to 52 percent of global emissions by 2030), they will remain fragmented, illiquid, and subject to moments of significant dislocation due to regulations and the technological and economic drivers of decarbonization.7

A detailed quantitative, transaction-linked understanding would enable better-informed investment decisions and a potential avenue to access competitive green-financing options. To capture these advantages and opportunities, players must accurately track the carbon exposure of their products and cargoes and connect it with their customers’ willingness to pay while also setting up the necessary physical processes and accounting protocols for compliance. In the future, this tracking could extend past carbon to a holistic view of multiple environmental, social, and governance (ESG) elements. First movers could also accumulate strategic volumes and scale to benefit from the price differentials that accompany the rapid expansion and uptake of green commodities and carbon markets. On a related note, as the green premium becomes more mainstream, it will provide traction to technologies (such as commodity tokenization) that enable more bespoke price discovery mechanisms and low-latency traceability.

For example, metals with different ESG and carbon footprint ratings, such as zero-carbon steel, have become considerably more popular. In the past 12 to 18 months, nine colors of hydrogen and ammonia have been introduced to the market, each with a differentiated production methodology.8

The combination of growing value pools and lower barriers to entry may lead existing players to pursue growth—particularly incumbent asset players that have yet to unlock their full potential. New entrants may also have added incentives to enter this space. While the competitive landscape can initially expand, scale could still be critical for success (especially at times of higher volatility and rapidly changing trade flows) for three reasons: it enables players to achieve better risk-adjusted returns (especially for new energies that need to be kick-started by large illiquid deals), to ensure global access to customers and optionality, and to secure more competitive financing.

Accordingly, scale will spur further industry consolidation. Large merchant traders and asset players will grow organically by taking away “flows” from smaller players and by growing in new asset classes. Asset players would increasingly be expected to acquire smaller players and, in the process, provide the risk capital and flows to supercharge growth. Meanwhile, smaller players would focus on “niches” that are less capital-intensive or more local. However, preparing for this phase of consolidation requires a rapid buildup of “smart scale”—in essence, focusing on scaling up a portfolio of alternatives in positions and products. In some cases, traders would have to make bold moves beyond the typical trading mandates. This pursuit of scale also has implications for business models: moving from a capital expenditure–based model to a more operating expenditure–based one would force traders to critically assess the trade-off between making one’s system more flexible and adding operating expenditures.

A number of players have been ramping up their trading businesses to capture their share of the growth in commodity trading, but their ambitions have been potentially limited by their trading platforms and operating models. This is mainly due to three reasons:

To develop a trading platform and an operating model that facilitate growth, players must first define their strategic ambitions and then make targeted investments to achieve the right mix of efficiency and agility to enable data-driven trading. For example, if a player’s strategic focus is on short-term trading, efficiency is critical. For the origination of customized and complex PPAs, a trading platform must be agile. And in prop trading, the increased integration of data into decision making will require both solid data governance and a best-in-class tech stack.

A successful trading platform requires several factors: an organization and operating model that incorporates agile principles where needed; the migration of technology applications to the cloud to unlock efficiency and reduce demand for talent; and a competitive employee value proposition to attract the in-demand technical specialists required for platform support.

The five success factors raise strategic questions for all classes of commodity trading players to consider. The following list of questions is not exhaustive but highlights some of the most pressing challenges for various sectors.

While the duration of this combination of cyclical bottlenecks, price transparency, and redefinition of commodity classes is uncertain, its effects will likely be felt beyond the short term and to different degrees in different commodities. In addition, many players will gravitate to one of three possible models, each with a different mix of the five success factors.

The digital enablement and convergence of markets, the prevalence of automation, and the migration of trading and optimization activity to short-term markets mean more players will be pursuing thinner margins. These developments will not only spur the addition of new at-scale players but also compel traders to ensure that their portfolios and customer access are more global and extend well beyond their legacy commodities. Players will explore both organic and inorganic options to achieve this growth. Incumbents of this model will use their access to competitive financing to attract flows from smaller players. The move toward third-party volumes in the portfolio will also enable a model that shifts from capital expenditures to operating expenditures. Integrated players will consider acquiring smaller trading units as an option to accelerate the buildup of trading capabilities.

In markets where scale is less relevant, lower barriers to entry are expected to attract multiple niche traders that target either regional or commodity-specific relationships. Specialists that enable new components of the carbon and ESG economy are one variation of this model. In the absence of barriers to entry, these players will need to develop and sustain a competitive edge based on either their customer centricity or their distinct technology and analytical capabilities. For example, in the biofuels feedstock market, players have carved out a niche by applying hard-to-replicate business models based on local insights, strong origination relationships, and acceptance of custom risks (such as those from innovative prefinancing agreements). As some of these fragmented markets become increasingly lucrative, niche traders could be viewed as acquisition targets by global smart-scale traders looking to add further scale and capabilities.

The cyclical nature of investment in commodity-based industries will result in supply and demand imbalances. Traders can capture value by taking positions that solve these imbalances. However, these types of positions (for example, battery storage leases) are not typically achievable through standard market access and therefore will create incentives for a breed of players willing to go outside traditional trading mandates. These tactical investors will possess a private equity mindset and use the strength of their balance sheets to take equity in illiquid physical positions aligned with their long-term views. In addition, they will possess a trading mindset that helps them better appreciate the nuances of the value of optionality associated with flexible assets, which in turn enables their capital allocation strategy.

Our analysis highlights the considerable impact possible through commodity trading in recent years and the underlying developments responsible. In the coming years, the effect of these developments and trends could be magnified, resulting in even more value at stake, which will then attract new players. An element of uncertainty surrounds these trends, especially with respect to timing. The combination of new players and uncertainty means winners need to think about both the size of their investment in these five success factors and their ability to move quickly.